Semitrailer Market Comprehensive Research Study 2029

-

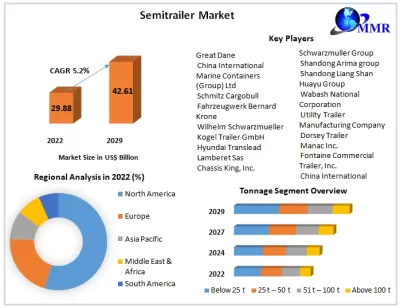

Semitrailer Market was valued US$ 29.88 Bn in 2022 and is expected to reach 42.61 Bn by 2029, at a CAGR of 5.2 % during a forecast period.

Market Size

- 2025 Market Value Estimate: USD 33.1 billion

- 2030 Forecast: USD 45.9 billion (CAGR ~6.7%)

- 2033 Projection: Up to USD 60 billion depending on continued tech uptake and cold-chain expansion

Overview

Semi‑trailers are road freight trailers without front axles—towed by tractor units—and are essential across logistics, construction, agriculture, and industrial sectors. Typical configurations include dry vans, refrigerated (reefer) units, flatbeds, lowboys, tankers, and specialized variants. Market innovation centers on electrified axles, aerodynamic designs, lightweight materials, smart telematics, and extended-length trailer formats.

To Know More About This Report Request A Free Sample Copy https://www.maximizemarketresearch.com/request-sample/29349/

1. Market Estimation & Definition

This market encompasses:

- Trailer Types: Dry van, flatbed, refrigerated, lowboy, tanker, extended/others

- Tonnage Classes: Below 25 t, 25–50 t, 51–100 t, above 100 t

- Length Categories: ≤45 ft, >45 ft

- Axle Counts: <3‑axle, 3–4‑axle, >4‑axle

- Application Sectors: Logistics & transportation, food, chemicals, cement, automotive, oil & gas, etc.

- Regions: North America, Europe, Asia‑Pacific, Latin America, Middle East & Africa

2. Market Growth Drivers & Opportunity

- E‑Commerce and Logistics Expansion: Rapid growth in express and full‑truckload logistics continues to lift demand for scalable trailer fleets.

- Cold‑Chain Boom: Rise in refrigerated trailer demand supported by food delivery and pharmaceuticals growth (reefer segment growing ~9% CAGR).

- Infrastructure Investments: Regional freight corridor projects—especially in Asia‑Pacific—spur trailer penetration.

- Tech Integration: Adoption of telematics, GPS tracking, aerodynamic kits, electric axles, and autonomous-ready bodies enhance operational efficiency.

- Sustainability Push: Fleets adopting lighter, fuel-efficient trailers to meet emission goals and regulatory thresholds.

3. Segmentation Analysis

- By Type:

- Dry van trailers lead in share (~35–55% depending on region).

- Flatbeds hold ~25%, driven by construction and heavy equipment transport.

- Lowboy trailers comprise ~12–13% (used for oversized or heavy machinery).

- Refrigerated units are fastest‑growing (CAGR ~8–9%) in the cold‑chain sector.

- By Tonnage and Length:

- Below 25 t tonnage leads (~33% share); 25–50 t is growing fast (~8% CAGR).

- >45 ft length category leads volume share; shorter trailers growing fastest (~7.7% CAGR).

- By Application:

- Logistics & transportation dominate (~40–50%).

- Food/cold‑chain segment growing fastest (~10% CAGR), followed by chemicals and cement industries.

4. Major Manufacturers

Leading semi‑trailer manufacturers globally include:

- Schmitz Cargobull (Germany)

- Krone (Germany)

- Schwanenhöfer / Kögel (Germany)

- CIMC (China)

- Wabash National (US)

- Great Dane (US)

- Utility Trailer Manufacturing (US)

These players lead in product innovation, global production capacity, and integration of advanced features like telematics and e‑axles.

Get More Info: https://www.maximizemarketresearch.com/request-sample/29349/

5. Regional Analysis

- Asia‑Pacific: Largest regional share (~44–56%), driven by China and India infrastructure build‑out, e‑commerce logistics and manufacturing growth.

- Europe: ~30–35% of revenue; strong standards and regulations push trailer innovation—especially telematics and lightweight design.

- North America: ~30–40% share; home to mature logistics operations and wide trailer length allowances.

- Latin America & Middle East/Africa: Smaller combined share (~7–10%), but see rising demand in logistics and cold‑chain sectors.

6. Country-Level Analysis (USA, Germany, China)

- United States: A mature marketplace with North America’s largest consumption. Integration of smart trailers and leasing models is common.

- Germany: Europe’s regional hub; premium trailer usage in automotive and manufacturing, plus strong growth in reefer and telematics-equipped units.

- China: Accounts for ~35% of Asia‑Pacific share; rapid adoption due to freight corridor development, cold‑chain expansion, and modular trailer production.

7. COVID‑19 Impact Analysis

The pandemic disrupted supply chains and logistics volumes in 2020–21, slowing production temporarily. However, the e‑commerce surge and cold‑chain transport needs during recovery drove trailer orders sharply in 2021–2022. Many fleets upgraded equipment and adopted smart trailer technologies as global trade rebounded.

8. Competitive (Commutator) Analysis

Market Structure: Moderately fragmented—with global OEM brands dominating large fleets and regional manufacturers serving local markets.

Trends in Competition:

- Telematics and fleet-management integration as differentiators.

- Emergence of electric-ready and aerodynamic trailer designs.

- Strategic alliances—like trailer makers co-engineering with autonomous truck developers.

- Vendors offering bundled financing/leasing to ease fleet expansion.

Challenges:

- Rising raw material costs impacting profit margins.

- Capital constraints for smaller fleet operators.

- Competition from rail/ship modal alternatives in long-haul routes.

Opportunities:

- Cold‑chain and food/e‑commerce expansion.

- Electric semi‑trailers and autonomous-ready chassis adoption.

- Extended‑length trailer use (above 60 ft) for high-volume freight corridors.

- Retrofit telematics and safety kits for used trailer fleet operations.

9. Key Questions Answered

Question

Answer

Market value in 2025?

~USD 33.1 billion

Forecast market size for 2030?

~USD 45.9 billion

Projected size by 2033?

Up to ~USD 60 billion depending on scenario

CAGR from 2025–2030?

~6.7%

Leading trailer type in 2024–25?

Dry van (~35–55%)

Fastest-growing sub-segment by type?

Refrigerated trailers (~9% CAGR)

Dominant application sector?

Logistics & transportation (~40–50%)

Largest region in 2024–25?

Asia‑Pacific (~44–56%)

Fastest-growing region?

Asia‑Pacific (~7–8% CAGR)

Key country markets?

China, U.S., Germany

Major trailer manufacturers?

Schmitz Cargobull, Krone, CIMC, Wabash, Great Dane, etc.

Press Release Conclusion

The global semi‑trailer market is entering a robust growth phase, expected to reach USD 45–60 billion by the early 2030s, propelled by logistics expansion, cold‑chain scaling, and integration of smart and electric-ready trailer technologies. Asia‑Pacific leads in volume expansion, while Europe and North America drive innovation through regulation-driven telematics adoption and sustainability mandates. Trailer makers that integrate aerodynamic, lightweight, and digital features—with flexible leasing or retrofit strategies—stand poised to lead the next wave of trailer modernization. As freight demands rise and regulatory pressures mount, semi‑trailers will remain pivotal to global cargo mobility and efficiency.

About Maximize Market Research:

Maximize Market Research is a global market research and consulting company specializing in data-driven insights and strategic analysis. With a team of experienced analysts and industry experts, the company provides comprehensive reports across various sectors, aiding businesses in making informed decisions and achieving sustainable growth.Contact Us

Maximize Market Research Pvt. Ltd.

2nd Floor, Navale IT Park, Phase 3

Pune-Bangalore Highway, Narhe

Pune, Maharashtra 411041, India

📞 +91 96073 65656

✉️ sales@maximizemarketresearch.com